We are glad to share with you that our recent conference paper “Optimization of Futures Price Forecasting and Trading Strategies Based on Clustering and Multi-model Fusion” from our MSAAI student Zhicong Song, which has been accepted in 2025 International Conference on Innovation Management and Information Systems (ICIIS):

- Z. Song, S.-H. Tsang and, T.-C. Hsung, “Optimization of Futures Price Forecasting and Trading Strategies Based on Clustering and Multi-model Fusion,” 2025 2nd International Conference on Innovation Management and Information Systems (ICIIS 2025), Shenzhen, China, April, 2025.

Paper Abstract

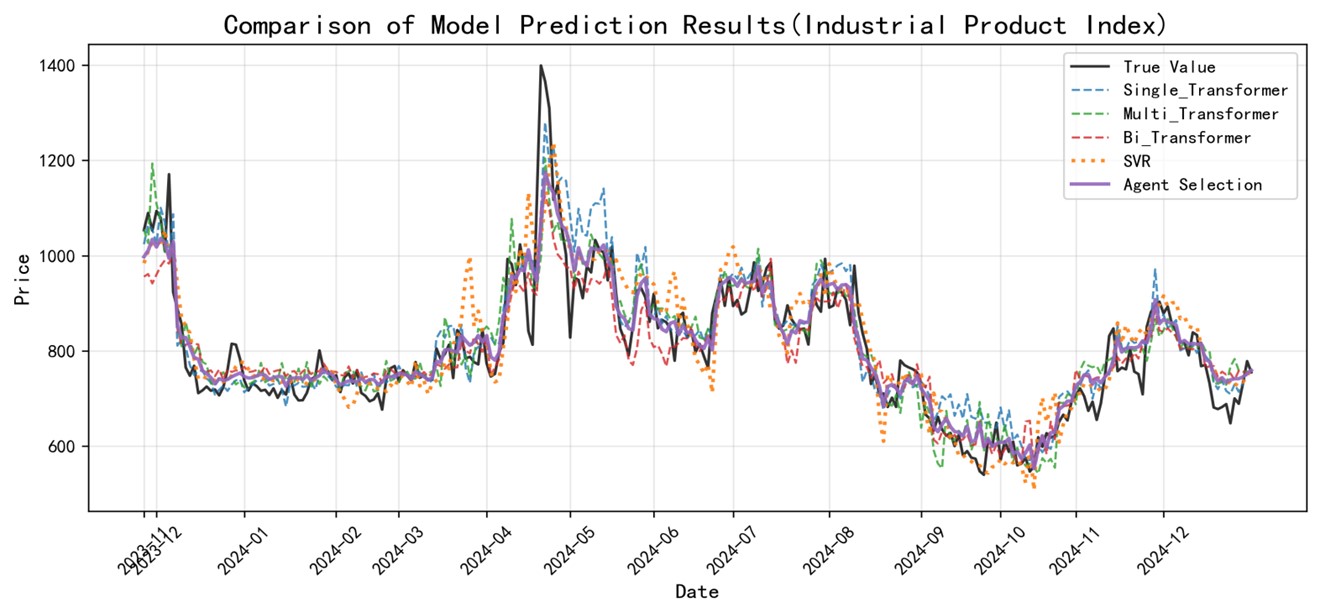

We’re thrilled to announce a groundbreaking real-time trading system designed to enhance futures price forecasting for 39 industrial futures listed on the China Commodity Exchange. The system starts by analyzing market conditions—like volatility and trend strength—using K-means clustering, effectively capturing diverse market behaviors.

It employs a smart forecasting strategy that combines Support Vector Regression for stable markets with Transformer models for highly volatile conditions. To optimize accuracy, a Deep Q-Network dynamically switches between these models based on current market states. Additionally, our system integrates with WeChat, providing users with immediate feedback on their trades for a more interactive experience.

In tests, our system achieved impressive results, with a Mean Squared Error of 0.0006 and an R-squared value of 0.86, demonstrating a high level of forecasting accuracy. We’re excited about the potential of this innovative trading system and its ability to enhance trading efficiency.

Some photos of the authors and papers

Futures Forecasting.

Model Comparisons for Futures Market Forecasting (Our Approach: Agent Selection).